So much of the country is living paycheck to paycheck. In my opinion, one of the contributing causes is the way people view their checking account balance. If you are like most people, you log into your bank account or stop by an ATM, see the balance staring back at you, and think:

“This is how much I have to spend.”

This assumption is very common, and it is one of the most damaging money mistakes someone can make.

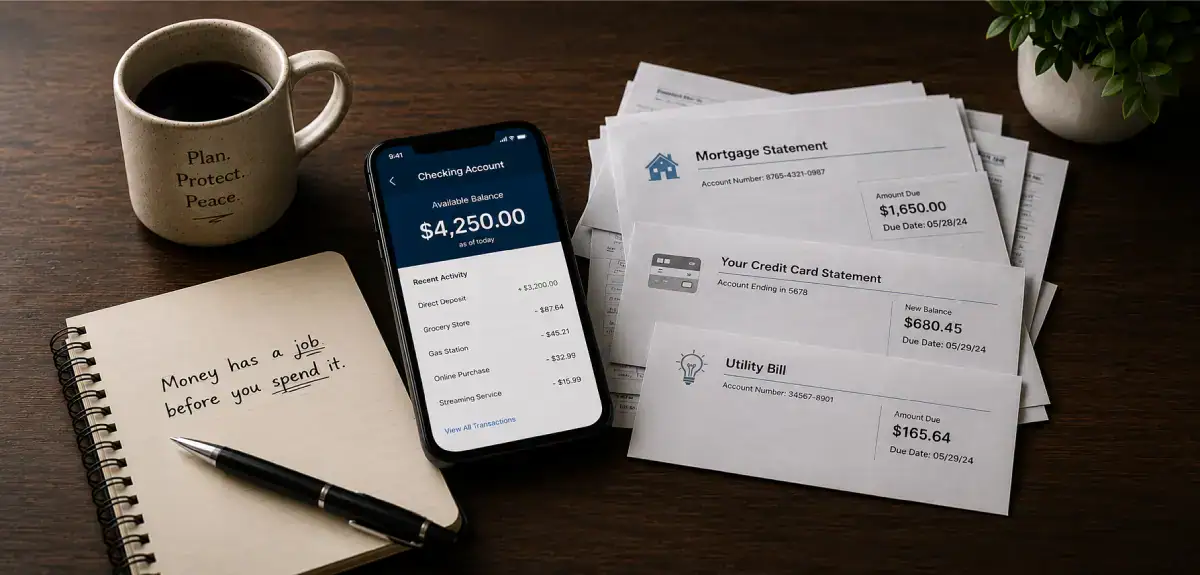

Your checking account balance does not tell you how much is available to spend. It reflects a moment in time by showing how much money is currently sitting there. Balance and availability are two very different things.

The Illusion of Available Money

Your checking account balance does not know:

- Your mortgage or rent is due in two weeks

- Your credit card statement has significant activity

- Your semi-annual property tax payment is due next month

- Your car payment will be pulled automatically by the end of the week

Much of the money sitting in your bank account is already spoken for.

Why This Trips People Up

Not everyone is careless with money. Many people are simply missing context.

When you rely on your checking account balance, you are forcing yourself to manage your finances based on memory and guesswork. This almost always ends badly – overdrafts, missed payments, and lower credit scores. Things can unravel quickly.

“I think my bills are covered.”

“I think I’ll be okay until payday.”

“I’ll figure it out later.”

This isn’t a system. It’s hope and hope is a terrible financial strategy.

Your Money Always Has a Job (Whether You Track It or Not)

This idea ties closely to the budgeting approach I shared in my recent post on How to Stick to a Budget (Even if You’ve Failed). I personally use a simple checking-account-based spreadsheet system that helps me see what my money is already allocated to, rather than relying on a single balance. I’ll be sharing that system in an upcoming post.

The point is that every dollar in your checking account already has a job:

- Housing

- Food

- Transportation

- Entertainment

- Savings (yes, this is a job)

- Unexpected expenses and reserves

You may want to be responsible, but if those jobs, and the amounts tied to them, aren’t clear, it’s easy to spend confidently today and feel surprised later when the money for an important payment is gone.

Why This Creates Stress

Even with a budget, a solid income, and the best intentions, financial stress will persist if your checking account balance is your primary decision-making tool.

Like I say above, the balance is a snapshot in time. Allocation is the full picture. When you don’t know what your money is already assigned to, every spending decision feels uncertain, and uncertainty creates stress.

Instead of asking:

“How much money do I have?”

Ask:

“What is this money already for?”

This shift isn’t about restriction or eliminating the things you enjoy. It’s about clarity. Knowing exactly what is safe to spend creates confidence and calm.

When uncertainty goes down, confidence goes up.

Start asking better questions. Start tracking your balance against real obligations. That simple shift can put you on a much more stable and intentional financial path.